Single women across the UK are potentially missing the opportunity to purchase a home according to data analysis by professional house buying firm, Open Property Group.

Following its recent Home Affordability Index, the firm has released a second insight summarising the realities of home ownership for single women across the UK, where house prices are suggested to need to drop by 48 per cent when purchased with a single income.

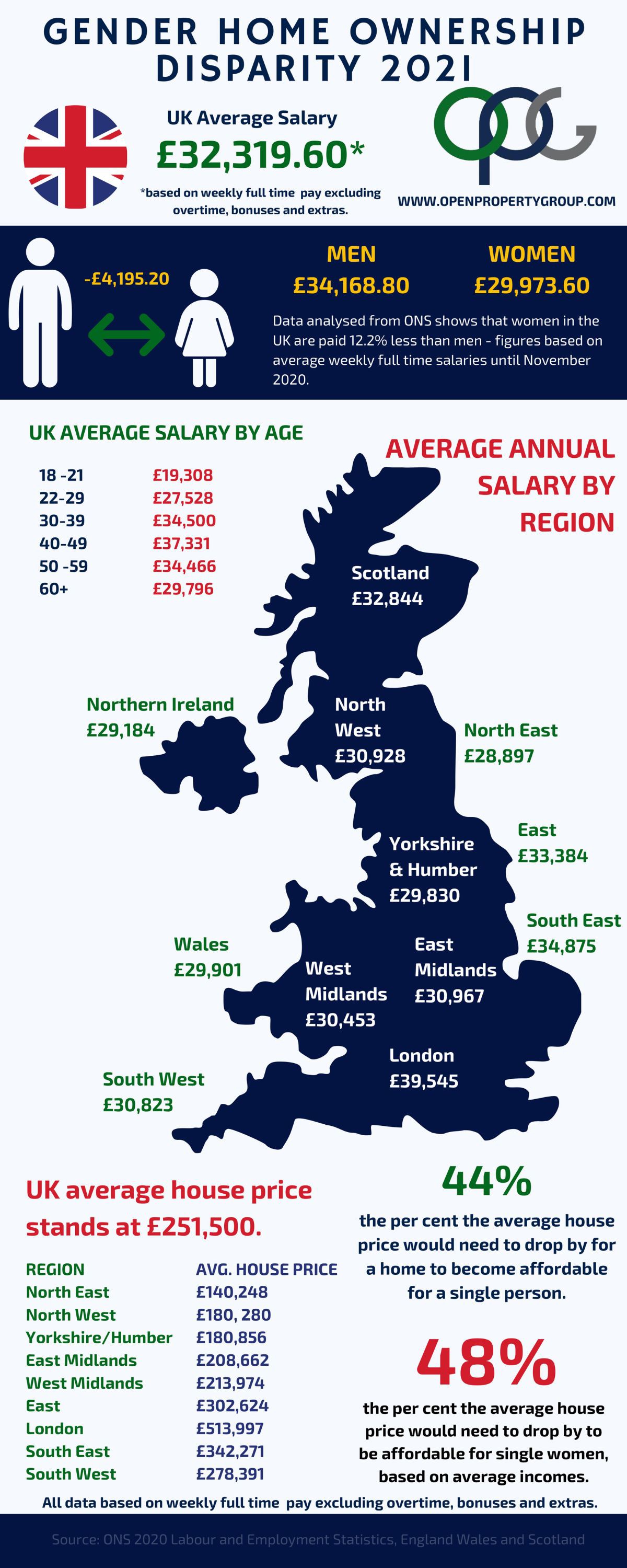

Findings from the research reveals a gender pay gap of 30 per cent between men and women in both full and part time roles. But for those working only in full time roles, the gap is less than half (12.2 per cent).

The National average of full-time employment income is £32,319.60 for a single person, and according to the data, the UK average house price stands at £251,500, suggesting prices need to drop to £141,398 (by 44 per cent) for a home to become affordable for a single person.

But based on average incomes for women, the average prices would need to drop to £131,134.50 (by 48 per cent).

Men however earn 5.72 per cent more than the national salary average at £34,168.80, meaning average house prices need to drop by 8% less (by 40 per cent) to £150,148.35.

The firm suggests on the face of it, is therefore unlikely that single women will be able to buy a home even based on regional salaries, unless they have substantial deposits to bridge the gap.

Salaries in London average at £39,545.28, but when the national average gender pay gap of 12.2 per cent below this is applied, a very different story is revealed.

When applying just a 5.72 per cent increase to this salary, the financial gulf women continue to face in 2021 becomes apparent.

A recent report by think tank Centre For London on how the pandemic has affected women’s earnings, shows a decline of 12.9 per cent, almost double that of men.

Open Property Group Managing Director, Jason Harris-Cohen commented:

“The gender pay gap does not show why women do not progress to certain jobs, which is often to do with lack of childcare support and parenting policies; and our research shows that more women are in part time jobs than men.

“With plans to continue to raise council tax and forging a Green Industrial Revolution targeted at men, news of freezing personal tax allowance from April 2021 at £12,570 until April 2026 does not help women.

“The Chancellor has failed to show foresight when delivering a budget that would put women on the map and address the necessary gaps in our economy in order to build a more egalitarian infrastructure,” says Jason.

Despite the government’s proposals of levelling up the economic disparity between the North and South through its 10-Point Green Industrial Revolution Plan, the firm suggests the Chancellor has done nothing to address the issue with the gender pay gap.

Jason added: “In the 25-34 age bracket, almost double the number of women than men have been made redundant and this is interesting as most women have children during this age bracket, as Pregnant Then Screwed says.

“When you look at furlough schemes and self-employment income support, women on maternity leave cannot apply as they do not qualify. Under the blanket of the pandemic, there has been a disproportionate number of convenient redundancies made towards females based on the fact that they may have childcare responsibilities and are more likely to be the primary caregiver.”

In the 2021 Budget, the Chancellor announced the Government Mortgage Guarantee Scheme which would see 95 per cent loan-to-value mortgages approved for first time buyers.

The sole purpose is to facilitate first time buyers getting on the property ladder, but fails to take into account people’s affordability for a mortgage and the 5% deposit they still need to raise.

Jason commented: “The problem is that the Chancellor has pledged a lot, but there is little by way of illustration in what it takes to buy a house.

“Firstly, saving a 5 percent deposit when you’re on a woman’s national average salary and renting, could be difficult. Secondly, there is zero support for all the costs associated with home buying such as stamp duty, solicitor fees, search fees, surveyors, and the time spent viewing homes, etc.

“There is very little by way of 90 per cent mortgage lender products out there at present, let alone 95 per cent. And this does not support the gender disparity women face who are disproportionately not offered mortgages based on the fact that they are more likely to become pregnant, made redundant and/or enter part-time work.

“These are all, rightly or wrongly, factors that lenders look at when offering mortgages.”

For more information on the latest affordability, please visit https://www.openpropertygroup.com/sell-house-fast/.

Thinking about selling? We’ll buy your property quickly!

No estate agent fees, no solicitor fees and choose a sale date to suit you!

Get your instant CASH offer below

![]()